Télécharger la dernière étude sur les indicateurs et chiffres clés du secteur terrestre/aéroterrestre

7.5 billion (-2.6%). This is the turnover of the land and airland-land defence and security sector represented by GICAT in 2019. With a historical core “Land Armament” that remains dominant.

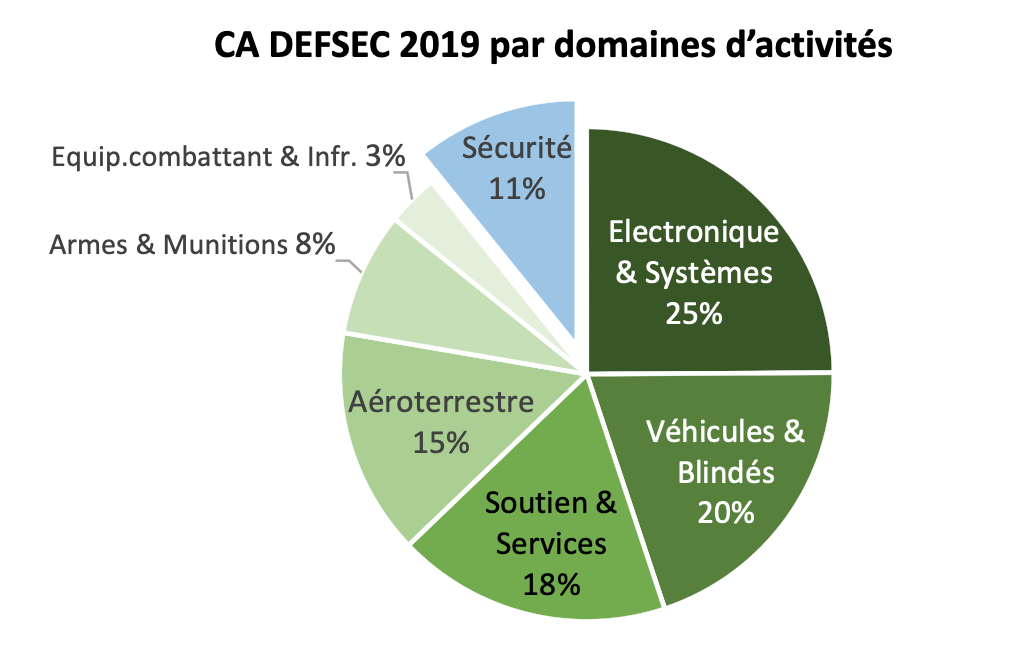

In 2019, activities related to “Electronics & Systems” represent 1/4 of Defence and Security revenues, followed by “Vehicles & Armor” (20%)

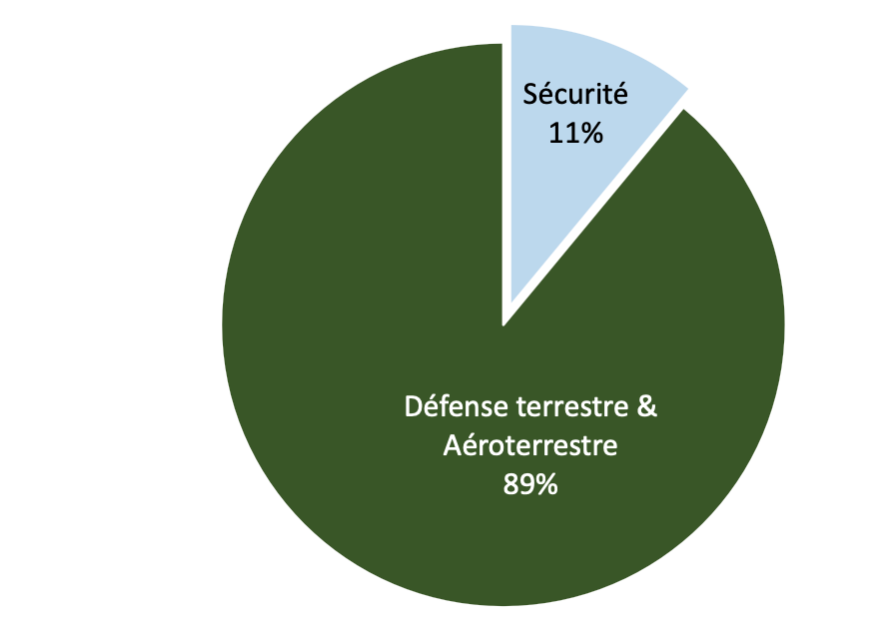

The “Security” share of total Defence and Security revenues is increasing, from 9% to 11%, driven in part by the activities of new members.

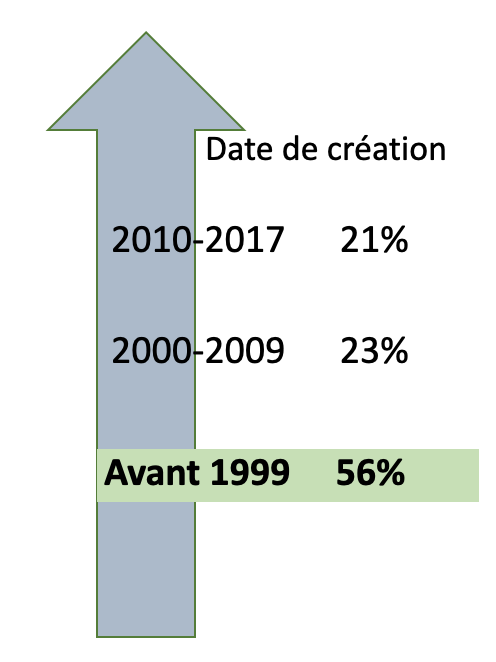

A coexistence of historical and more recent companies. On the one hand, 56% of member companies and 56% of SMEs were created before 1999. On the other hand, 21% of member companies have been in existence for less than 10 years (a figure that is constantly increasing: 19% in 2019, 14% in 2018).

The sector represents more than 24,000 direct jobs and almost as many indirect jobs.

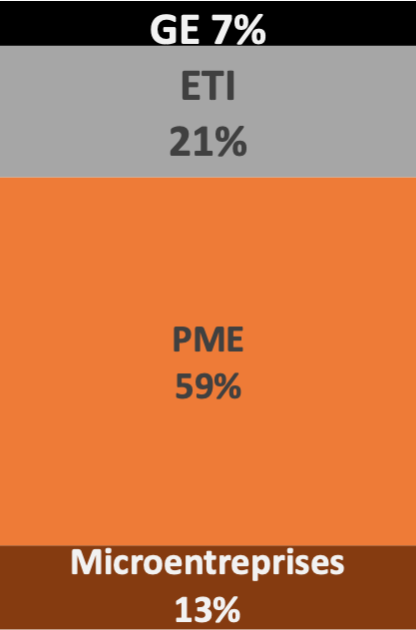

In 2019, GICAT included more than 7% of large groups, nearly 21% of ETIs, nearly 72% of SMEs and Microenterprises.

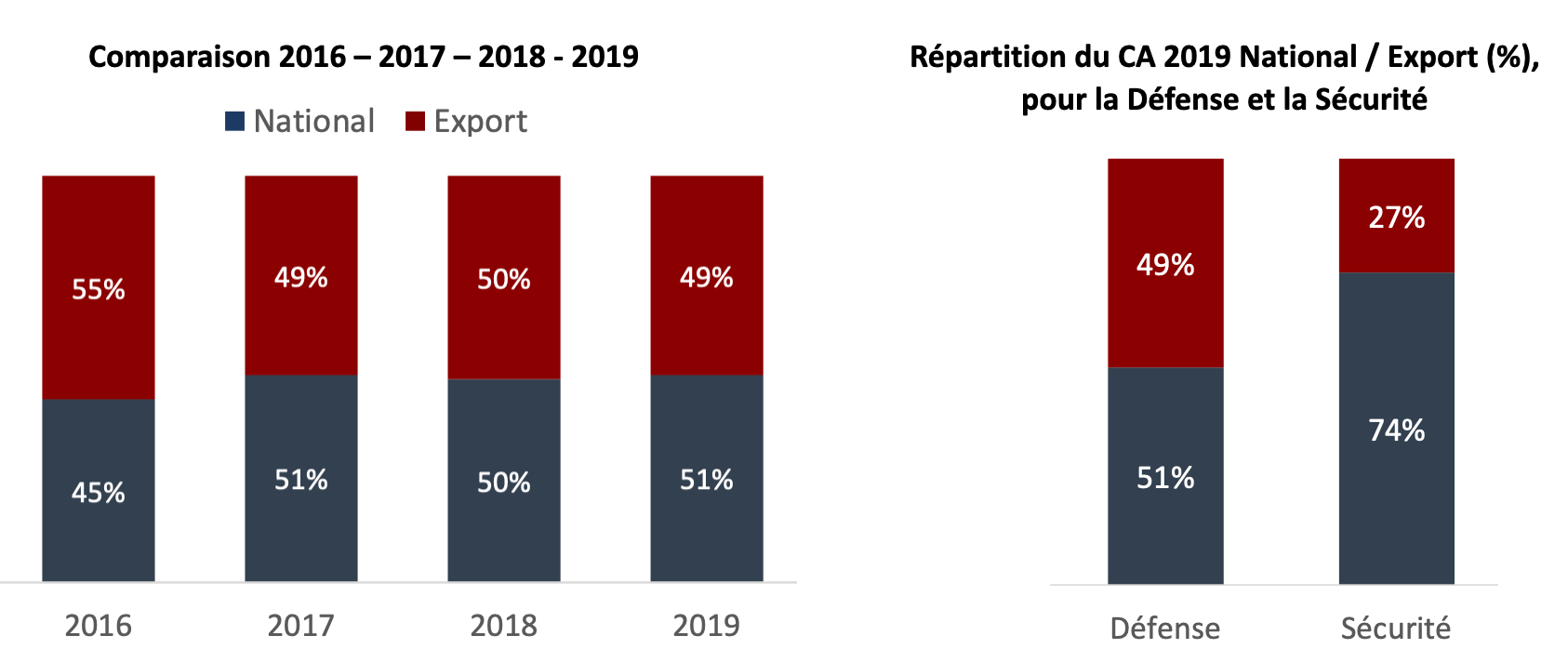

A stable “Europe” export share (23%), with a return to growth in export sales made in North Africa, Near and Middle East (share of 50% of export turnover 2019 against 45% in 2018).

Confirmed growth in the share of sales to sub-Saharan Africa (7% in 2019 compared with 5% in 2018 and 1% in 2017).

For the first year since 2017, decline in the share of exports to the Asia-Pacific region (16% in 2019 versus 21% in previous years).

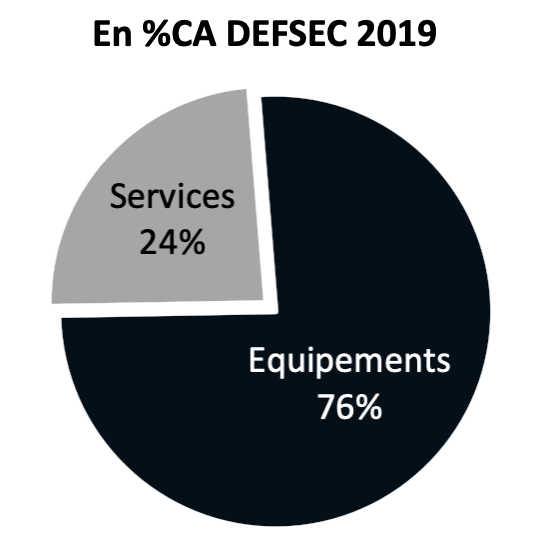

A year focused on equipment production.

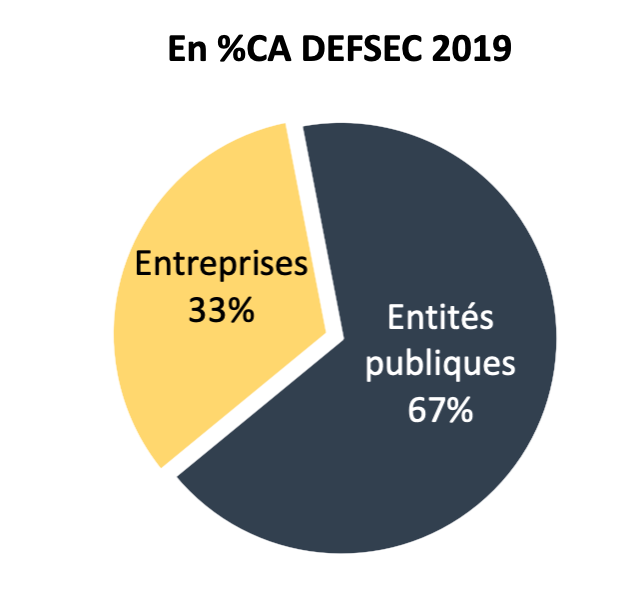

Our customers remain mostly public entities (67% of revenues).

The land and airland-land Defence and Security sector remains very present internationally, with a stable share of exports to our European partners.